简体中文

简体中文

At the invitation of the organizing committee, Dai Bin, President of the China Tourism Research Institute, went to Tianjin on September 2 to attend the 2023 Global Travel Business Conference. He delivered a keynote speech on the current tourism economic situation, policy orientation, and key tasks. For the first time, he released quantitative research results on the impact of the epidemic on the tourism industry in the past three years, main data on summer tourism in 2023, and research results on the old pattern and new order of the tourism industry. The full text is as follows.

01

The tourism economy has entered a new channel of recovery and prosperity is expected

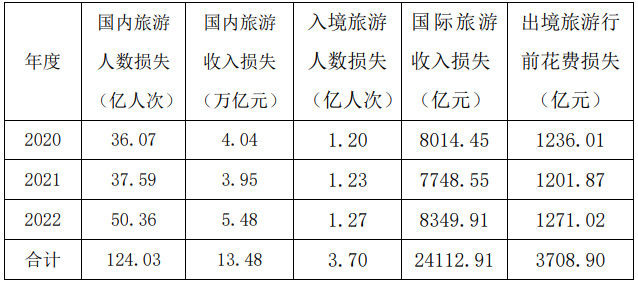

Over the past three years, the data of the deep depression has been engraved into the annual rings of tourism development in the Republic, becoming an eternal memory in the industry. The China Tourism Research Institute (Data Center of the Ministry of Culture and Tourism) compared the potential growth rates of domestic and inbound/outbound tourism markets before the epidemic, and for the first time, modeled and calculated the economic losses of national tourism from 2020 to 2022. The number of domestic tourists decreased by 12.403 billion, and the total loss of domestic tourism revenue was about 1.348 trillion yuan; The number of inbound tourists decreased by about 370 million, resulting in a loss of international tourism revenue of approximately 362.06 billion US dollars, equivalent to 2.41 trillion yuan. Adding in the pre departure expenses incurred by outbound tourists, such as purchasing domestic airline tickets, insurance, pre departure equipment, visa processing, and transportation and accommodation, the loss of pre departure expenses for outbound parades is approximately 370.9 billion yuan. In the past three years, the national tourism consumption has lost at least 16.27 trillion yuan, equivalent to 12.8% of the total retail sales of consumer goods in China during the same period, with an average reduction of approximately 3841 yuan in tourism consumption per person per year.

Table 1 Estimation of Potential Losses in the Tourism Market from 2020 to 2022

According to the Tourism Satellite Account (TSA) law, China's tourism industry has suffered a total loss of approximately 10.95 trillion yuan in added value over the past three years, with an average annual decrease of 1.27 percentage points in the nominal GDP growth rate. According to the estimation of per capita GDP in the industry, the number of tourism employment in China has shrunk from 28.75 million to around 16 million, and 43.4% of tourism practitioners have temporarily or permanently left the tourism industry. After three years of deep recession, the tourism industry has faced the most difficult challenges and the longest recovery in history, demonstrating the strongest resilience and unwavering confidence.

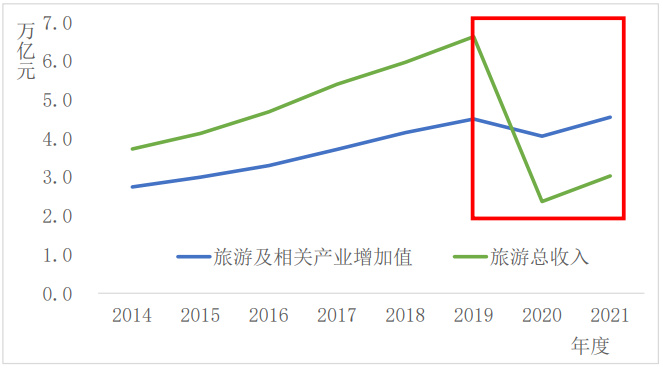

Figure 1: The added value and total tourism revenue of tourism and related industries according to statistics from relevant departments of the National Bureau of Statistics

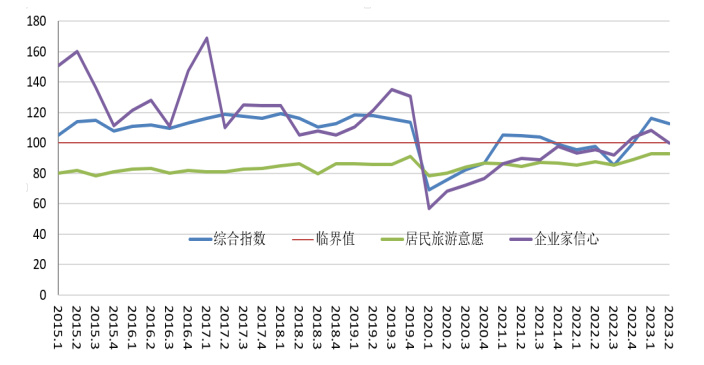

Affected by multiple favorable factors such as relaxed policies on residents' travel and contact consumption, stable and positive macroeconomic conditions, and central and local measures to promote consumption, the tourism economy in the first half of 2023 has entered a comprehensive recovery new channel of "stable opening and high growth, accelerated recovery, simultaneous increase in quantity and price, and strong supply and demand". Whether it is residents' willingness to travel, tourist satisfaction, entrepreneurial confidence, comprehensive prosperity index of tourism economy operation, or travel distance and destination recreational radius, they have all reached or are close to the level of 2019.

Figure 2: Tourism Economic Prosperity Index from Q1 2015 to Q2 2023

The recovery of the summer tourism market continues to accelerate, with most destinations receiving the highest number of tourists in history. According to the China Tourism Research Institute (Data Center of the Ministry of Culture and Tourism), the number of domestic tourists in China during the summer of 2023 (June August) will reach 1.839 billion, achieving a domestic tourism revenue of 1.21 trillion yuan. With the continuous increase in market heat, the prosperity of the tourism industry has begun to spread from upstream resource providers such as scenic spots, catering, accommodation, and transportation to the travel service industry represented by ticketing agents, channel distribution, tour guides, and team leaders. The flow of customers has also begun to spread from short distance to long distance destinations. Affected by the high demand for graduate studies, parent-child care, summer vacation, health care, and vacation tourism, urban and rural residents are more willing to stay in their destination for a longer period of time. According to big data monitoring, the summer travel time of tourists nationwide has significantly increased, with a year-on-year increase of 36.77%.

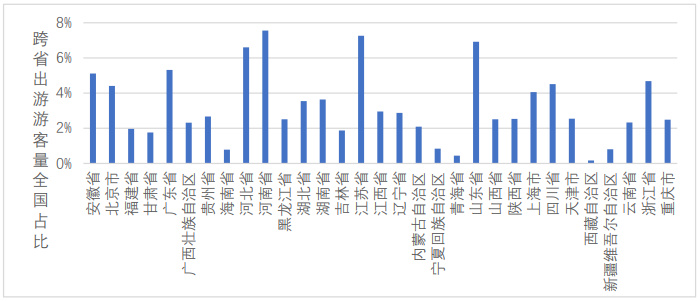

Figure 3: The proportion of cross provincial tourists traveling between provinces in the summer of 2023 in China

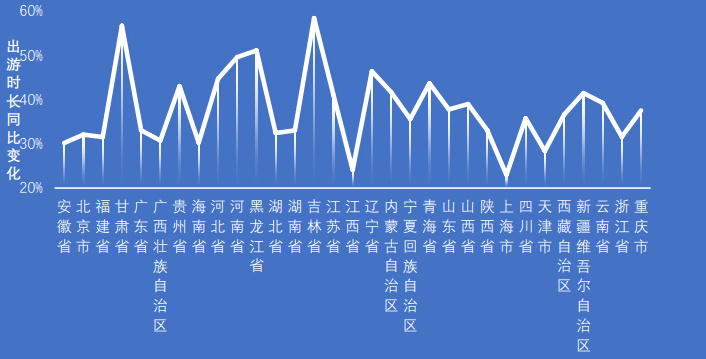

Figure 4: Travel radius and duration in each province during the summer of 2023

Multiple, multidimensional, and continuous data indicate that the tourism economy has irreversibly moved from depression to recovery. We have reason to hold positive and optimistic expectations for the upcoming Mid Autumn Festival, National Day holidays, and the tourism economy throughout the year. With the accumulation of entrepreneurial and innovative momentum in culture, art, technology, education, and the release of more favorable policy effects, the tourism economy is about to enter a prosperous period.

02

The old pattern of the tourism industry is dissolving, and a new order is beginning to be constructed

The epidemic has disrupted the balance between online and offline markets, and the traditional offline tourism ecosystem, especially inbound tourism services, has been more severely impacted and deeply affected. In 2003, the "SARS" epidemic promoted the online substitution of the tourism market to a certain extent. Qunar, Tongcheng, Tuniu, Mafengwo, Mummy Donkey and other online travel businesses were able to rise rapidly. The COVID-19 also promoted the acceleration of tourism transactions from offline to online. New media such as Tiktok and Xiaohongshu played a more obvious role in tourism marketing, customer solicitation and transactions, and showed a strategic entry trend. In contrast, due to the high sunk costs of rigidity and the increase in non-contact transactions with tourists, most offline tourism enterprises still need a longer time to repair their supply chain and cash flow. The epidemic has also disrupted the market balance between local and non local supply systems, and the repair of the tourism industry chain from remote destinations to the resource side is relatively lagging behind. During the epidemic, the shrinking demand for tourism has been released nearby, and leisure products such as urban micro tourism, urban reading, weekend boarding, Shanghai style urban archaeology, exquisite camping, hotpot buses, and water tea houses are selling well. As the operational advantages of tourism enterprises shift from the resource side to the source side, the dominant role of population base in the distribution of tourism market entities and the evolution of business models becomes more prominent. Recently, more local residents have applied for and verified the tourism consumption coupons and coupons that have been launched in various regions, which has accelerated the localization of tourism market entities to a certain extent. Relatively speaking, tourism enterprises in remote destinations lack the basic market support of local customer sources, resulting in a relatively lagging market recovery. The sense of gain and supply chain recovery of market entities are also relatively low. The epidemic has also disrupted the market equilibrium between existing operations and incremental investment, making deleveraging and repairing the balance sheet a top priority for tourism market entities. Due to the impact of the epidemic, the balance sheets of the vast majority of tourism enterprises have significantly declined, and the debt ratio has significantly increased. After entering the market recovery period, tourism enterprises are more inclined to repair their balance sheets through separation of main and auxiliary businesses, sale of heavy assets, branding, and management output, rather than expanding investment and increasing leverage. The current upward recovery of the tourism economy is mainly driven by consumption, while the movement of the production possibility curve is more driven by investment and innovation. How to solve the dilemma of "government cannot invest and enterprises are unwilling to invest" in the tourism industry is the current policy direction and a key task to promote high-quality development of the tourism industry.

New driving forces for resource development are accumulating, and a new pattern for destination construction is being constructed. As mass tourism moves from its initial stage to a new stage of comprehensive development, the diverse and high-quality consumer demand is beginning to force innovation and structural optimization on the tourism supply side. The simple reproduction model of "a sea of people eating dividends and collecting tickets by surrounding mountains and waters" will be replaced by a capital and technology driven circuitous production model. Tourism destinations of different spatial scales should shift towards new driving forces such as technological applications, cultural creativity, scene creation, product research and development, and human resources based on natural resources such as mountains, waters, forests, fields, lakes, grasses, sands, and cultural resources such as archaeological sites and cultural museums, and thus extend the tourism industry chain and cultivate a diverse and symbiotic tourism ecosystem. In the new era of comprehensive development of individual, independent and self-help mass tourism, we cannot be confined to the traditional small tourism model to promote the high-quality development of tourism in the new era. We must rely on the development achievements of the "Chinese Dream" of Chinese path to modernization to promote national rejuvenation and people's happiness, including infrastructure and public services such as transportation, municipal administration and people's livelihood, as well as modern industrial, agricultural, commercial, logistics and other business environments, and incorporate tourism into national strategies such as national parks and national cultural parks, so as to empower each other and go in both directions. Above the landscape lies life, while the purpose of tourism is the sum of the living environment. We must deeply implement the people-centered concept of mass tourism development, continuously improve tourism infrastructure and public services, open more urban parks, suburban parks, cultural and museum venues, educational institutions, and public leisure spaces to tourists, allow people to freely walk on this beautiful land, and make every city, every block, and every village a new space for a beautiful life that is both nearby and far away, shared by hosts and guests.

Enhance factor productivity and corporate innovation, and build a new competitive landscape for the tourism industry. Travel service providers represented by travel agencies, online travel agents, and tour guides, tourism accommodation providers represented by hotels and homestays, and tourism leisure spaces represented by scenic spots, resorts, and neighborhoods are typical market entities in the tourism industry. The strength of their competitiveness directly determines the process of the tourism industry from recovery to prosperity. Encouraging market entities to seek long-term competitive advantages rather than short-term monopoly positions, and continuously improving the overall productivity of the tourism industry through research and development investment and digital transformation in competitiveness, forming a new pattern of "collaborative innovation of tourism groups, specialized operation of medium-sized enterprises, and digital survival of small and micro enterprises", should be the value orientation of tourism policies in the recovery stage. The tourism system should not only be satisfied with holding conferences, issuing documents, and branding, but also take practical and effective measures to lead market entities in content creation, scene construction, product research and development, and quality improvement, so that grassroots tourism workers and frontline practitioners such as tour guides, leaders, study tour guides, banquet customizers, etc. have reasonable salary and good social reputation.

03

Tourism policies shift towards supply chain restructuring and the cultivation of new business models, with a focus on high-quality products and services

With the accelerated recovery of the tourism market driven by demand, tourism policies need to shift towards supply chain restructuring and industrial ecological cultivation. In the past three years, the central and local governments have introduced various relief and assistance policies, which have given market entities a certain sense of gain. It should be noted that due to the fact that relief policies often target transaction indicators, enterprises with larger turnover/transaction volume receive more support. Cultural and tourism consumption vouchers are also mainly invested in large platform merchants and top enterprises, objectively leading to a "winner takes all" situation for top enterprises. Local, private, and small and micro enterprises often sigh at the policies. From the data of the first half of the year and summer, large platform operators have already achieved profitability, while small and micro tourism enterprises are facing pressure from declining revenue and high platform commissions. From now on, tourism industry policies should pay more attention to the restoration of the industrial chain and the development of the industrial ecology, strive to enhance the sense of achievement of small and micro enterprises, and encourage the growth of specialized and new entrepreneurial enterprises in segmented tracks. To prevent top enterprises from using policy effects to accelerate market share, thereby forming a situation where the market is still recovering and industrial monopoly has already been established. Encourage top enterprises to focus on their main business, weaken unrelated diversified businesses, use "closed-loop" strategies cautiously, guide OTA platforms to appropriately reduce supplier commissions, and provide more growth opportunities for small and micro enterprises and startups.

Guide local governments to attach importance to the capacity restoration of market entities and the enhancement of industrial investment capabilities. With the rapid recovery of the tourism market, the enthusiasm for attracting investment and establishing industry funds in various regions is very high. Government leaders at all levels frequently visit the top 20 tourism groups to complete the task of attracting investment. Unfortunately, due to the decline in the land balance ability of local governments and the funding capacity of platform companies, coupled with the need to restore the investment willingness of market entities, a situation has objectively formed where "the government cannot invest and enterprises dare not invest". From the perspective of the capital market, the number and amount of debt financing for A-share listed tourism companies in the first five months decreased by 53.0% and 56.5% year-on-year, respectively. We have noticed that cities such as Xi'an, Luoyang, Zibo, and Rongjiang have shifted their tourism focus from attracting investment towards the B-end to activating the market towards the C-end, effectively alleviating the cash flow difficulties of local tourism enterprises and boosting the enthusiasm of out of town tourism enterprises to invest. Millions of policies, the first one in the market. Local governments, especially those in the cultural and tourism sectors, respect market rules and cannot always rely on resources, land, and preferential policies to attract investment. They cannot always attract attention with short-term popularity and artificial traffic, but should attract investment with stable growth in demand, consumption, and market. With high-frequency consumption and a stable growth market, capital will have confidence, and talent and technology will also follow. The tourism economy will eventually enter a benign development track of "demand driving supply, supply creating demand".

Tourism policies should shift from short-term market recovery to long-term high-quality development, and closely monitor the transmission of macroeconomic fluctuations to the tourism sector. Due to the low base of various indicators in the tourism market in 2022 and the concentrated release of inhibitory demand this year, the tourism market is accelerating its recovery, and the performance of various indicators is impressive. However, it is also easy to conceal some structural problems and long-term risks. The tourism industry is a sensitive industry to sudden events and also a countercyclical industry for economic development. It is expected that from 2024 onwards, the policy effect of promoting tourism consumption will further decrease, and the growth rate of various indicators will return to normal. The tourism economy will shift towards an endogenous growth model driven by capital, technology, digitization, and cultural and creative industries. Each region should analyze the quarterly economic situation in the cultural and tourism fields, predict in advance the problems that may arise after the market growth slows down, and formulate reserve policy plans, with the focus on ensuring the "reasonable growth in quantity and effective improvement in quality" of the tourism economy. In the process of promoting the recovery and high-quality development of the tourism market, the departments of joint development and reform, commerce, market supervision, statistics, etc. will focus on strengthening competition orientation and risk warning, restricting industry concentration, industry monopoly, and non market brand creation.

Coordinate the development of inbound and outbound tourism markets, build a world tourism community, and continuously enhance global discourse power and industrial influence. Whether before or after the epidemic, China has been a key force in the prosperous development of the world tourism economy. From the current situation, the role and impact are still limited to the position of the largest outbound source country and the importing country of tourism service trade. Although China no longer pursues, nor can it pursue, maintaining a trade surplus in tourism services with any country or region at any time, it does not mean giving up the strategic goal of revitalizing inbound tourism. Inbound tourism has always been a barometer of a country's tourism image, destination development, and corporate innovation. The determination to develop inbound tourism has never wavered, and confidence has never been lost. The policy points that can be expected at present include but are not limited to: establishing a central level tourism deliberation and coordination mechanism, increasing government coordination efforts, and promoting dynamic balance of inbound and outbound tourism; Positioning the expected indicators for inbound tourism in 2024 as' returning to the same period in 2019 '; Develop and implement the 'Outline for Revitalizing Inbound Tourism and 2035 Long Range Objectives'. To revitalize inbound tourism, it is necessary to pay attention to policies such as diplomacy, immigration, civil aviation, tax exemption, payment, and the Internet. It is also necessary to pay attention to national tourism image publicity and market promotion, but also to tourism infrastructure construction, product research and development, and service quality. In the era where content is king, without high-quality products and sincere services, it is impossible to attract foreign tourists by relying on a few eye-catching conferences, exhibitions, roadshows, and soft articles. We need to strengthen the construction of high-frequency and fine-grained market data, give full play to the frontline role of overseas tourism offices and cultural centers, make good use of the international tourism organizations initiated and established by China, and promote their outward development rather than seeking advantages internally. Guided by the Global Civilization Initiative and the concept of great power diplomacy, we actively advocate and pragmatically promote the construction of a world tourism community, building a value foundation and spiritual momentum for the prosperity and development of the global tourism industry.

.jpg)

Author | Dai Bin

Manuscript Review | Yang Liqiong

Source | China Tourism Research Institute (Data Center of the Ministry of Culture and Tourism)

Please indicate the author and source when reprinting

ALL RIGHTS RESERVED:CHINA TOURISM ACADEMY (Data Center ofthe Ministry ofCulture and Tourism)

ICP备案: 京ICP备2021001490号-1